Mortgage Tips for 1099 Self Employed Homebuyers

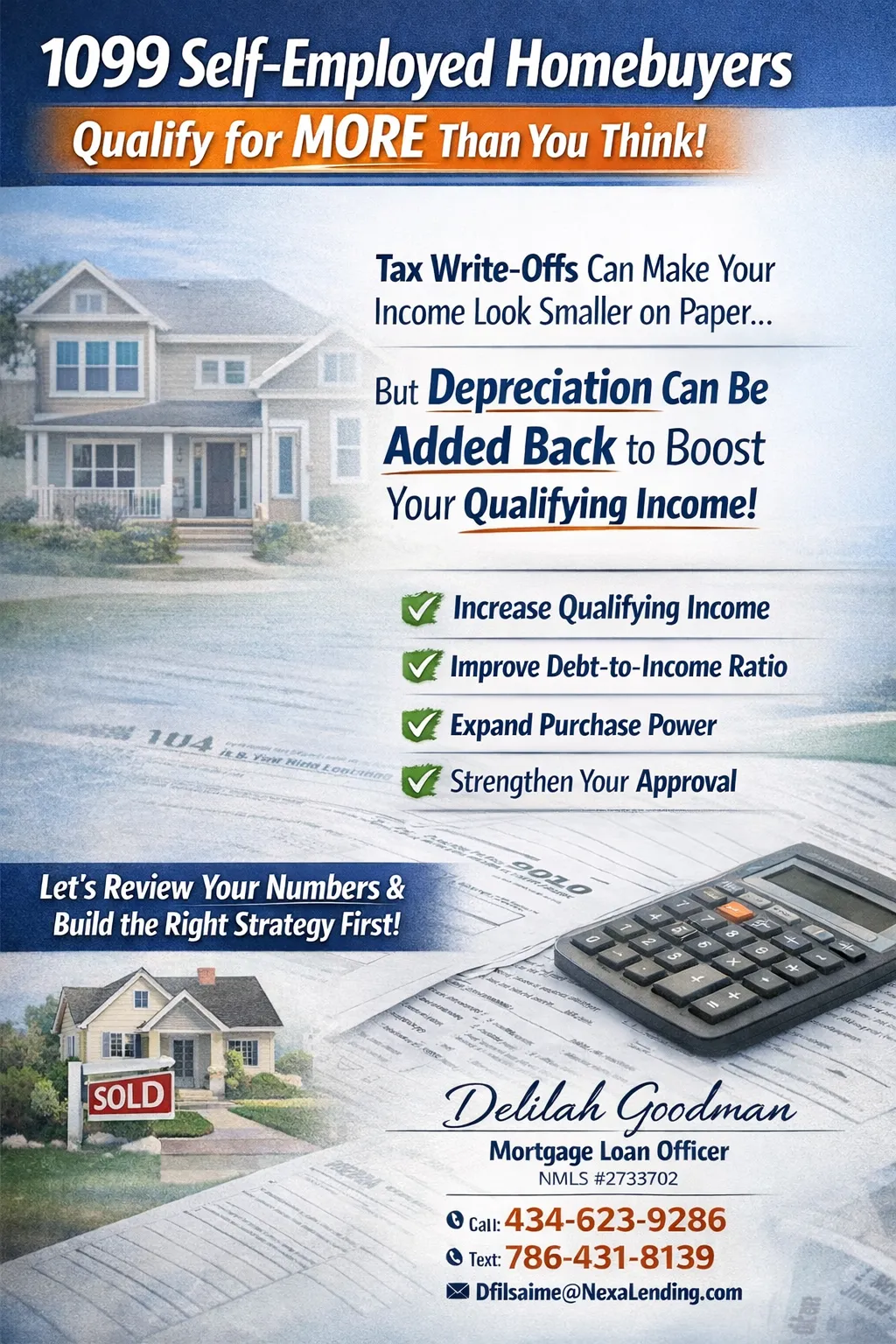

When you’re self-employed and paid on a 1099, qualifying for a mortgage works differently than it does for a traditional W-2 employee. The key factor lenders look at is taxable income, not just the gross revenue your business generates.

Many self-employed borrowers run into a common problem:

They do a great job reducing their taxable income through business write-offs, but those same write-offs can make their income appear lower on paper when applying for a mortgage.

This is where working with a mortgage broker and experienced loan officer becomes extremely important.

How Depreciation Helps Self-Employed Borrowers

Certain expenses on your tax return—especially depreciation—can often be added back to your income when we calculate your qualifying earnings for a mortgage.

Depreciation is a non-cash expense. It reduces taxable income for IRS purposes, but it doesn’t actually reduce the money you earned.

Because of that, underwriting guidelines for many mortgage programs allow us to add depreciation back into your income calculation, which can significantly increase the income used to qualify.

For example:

• Your tax return might show $80,000 in net income

• But you also claimed $25,000 in depreciation

When structuring your mortgage application, we may be able to use:

$105,000 in qualifying income instead of $80,000

That difference can directly impact:

Your loan approval

Your maximum purchase price

Your debt-to-income ratio

Your monthly payment comfort level

Why Structuring the Mortgage Matters

Many banks simply take the numbers from your tax returns and run them through a system.

A mortgage broker takes a more strategic approach.

My role is to review your full financial picture and structure the loan correctly before it ever reaches underwriting.

This includes:

• Identifying eligible add-backs like depreciation

• Reviewing two years of tax returns strategically

• Calculating income the way underwriters actually evaluate self-employed borrowers

• Determining whether conventional, bank statement, or other programs will work best

Small adjustments in how income is analyzed can mean the difference between:

Denied vs. Approved

Lower purchase power vs. Higher purchase power

Higher stress vs. A smooth closing

Why This Matters for 1099 Borrowers

Self-employed buyers are often overqualified financially, but under-represented on paper because of tax strategies used to reduce their tax burden.

A mortgage loan officer who understands how to properly analyze self-employed income, depreciation, and business deductions can help ensure your financing reflects your true earning power.

That’s why it’s important to speak with a mortgage professional before starting the home search.

When your loan is structured correctly from the beginning, you shop for a home with confidence, clarity, and stronger approval terms.

Delilah Goodman

Mortgage Loan Officer | NMLS #2733702

O: (434) 623-9286 | C: (786) 431-8139

[email protected]